FRANK O’BRIEN/PETER MITHAM

Other

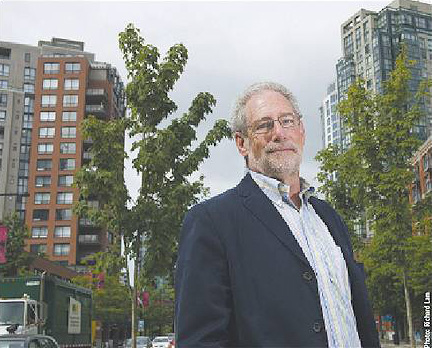

Michael Goldberg, professor and dean emeritus with the Sauder School of Business at UBC: ease regulations to create more higher-density, lower-cost housing in Metro Vancouver.

A sharp drop in Metro Vancouver housing sales in July and an apparent stall in rocketing price increases has shocked residential investors, but a top University of British Columbia (UBC) professor says local politics should help keep supply low and prices rising. Michael Goldberg, professor and dean emeritus at UBC’s Sauder School of Business, argues too-restrictive zoning and the NIMBY factor mean not enough new homes are being built, especially around rapid-transit hubs. Goldberg says the solution for bringing down the cost of development and housing in Vancouver lies in reduced planning regulation and allowing property developers more leeway to construct taller buildings faster. “It can take six years to get rezoning for a highrise tower in Vancouver,” said Goldberg. Lifting restrictions and allowing developers to build higher-density projects would result in an oversupply of homes and, subsequently, lower prices, he said. “We should be tapping the greed factor [of developers].” Goldberg said municipalities and residents voice support for higher density but, when projects are planned, politicians often cave in to local “not-in-my-backyard” protests and shelve the projects. The professor says Vancouver council should be pushing for highrise condominium towers along major commercial strips, such as Dunbar and West 41st in Vancouver, and next to Skytrain and Canada Line stations. Vancouver council voted May 10 to increase density in the Cambie corridor to 12 storeys, but Goldberg said much higher buildings are needed both there and around the Oakridge Centre and Marine Drive transit stations. “It’s ludicrous,” he said, noting that the Commercial Skytrain Station, a major transit hub, has no adjacent high-density housing and only a small food-anchored shopping mall. He added that the Cambie Street/Broadway Avenue Canada Line Station has attracted only a new retail complex. “None of the transit stations are linked underground to residential or retail buildings,” he said. The City of Vancouver should also abandon regulations that protect “views of the mountains,” said Goldberg. He considers the mountains to be high enough that buildings are not going to interfere sufficiently with the views to bother with a regulation. Building-height limits, too, should be dropped across the Metro region, according to Goldberg. He argues that market condition should dictate the height of buildings, not planning regulations. “Seventy per cent of the residential in Vancouver are single-family, detached houses,” Goldberg said, “but the trend is toward smaller homes,” due to empty nesters and young people who want to live in urban centres. Judging from July stats, the trend toward higher density and lower prices may have already begun. According to Canada Mortgage and Housing Corp., multiple-family housing starts are up in Vancouver and across the region. In the first six months of 2011, 1,473 strata apartments or townhomes broke ground, up from 1,373 in the same period last year. At the same time, less than 300 new detached houses were started. Buyer’s market looms Re-sales of homes across Metro Vancouver had been slowly declining for four straight months, but July sales slumped 21 per cent from a month earlier to around 2,500 units. Homes for sale, meanwhile, shot up 23 per cent from last summer as buyers try to cash in on average prices topping $630,000. As of July, the typical price for a detached house in Greater Vancouver was $898,886. It soared over $2 million on Vancouver’s west side and to more than $1 million in Richmond and most of the North Shore. “The number of homes listed for sale in the region has increased each month since the start of the year,” said Rosario Setticasi, president of the Real Estate Board of Greater Vancouver. As of this summer, listings were at 15,200, an indication that buyers are gaining the upper hand. In the Fraser Valley, July sales were down 17 per cent from June, and a 24 per cent spike in listings meant that more than 10,000 homes are listed for sale but only 1,300 are selling per month. Fraser Valley Real Estate Board president Sukh Sidhu calls it a “buyer’s market,” noting it now takes an average of 65 days to sell an Abbotsford condo, the least expensive home in the Fraser Valley. Speculative builders Speculative residential developers remain bullish on the new-condo market, however, according to an August survey released by market research firm MPC Intelligence Inc. MPC is waving red flags, though, warning of a glut in some markets if pre-sales don’t accelerate. MPC’s Lower Mainland survey showed that during the first half of 2011 a total of 87 multi-family projects or project phases started marketing in Metro Vancouver. These projects added a total of 6,410 units to the market. By the end of June, 57 per cent of these units were reported sold. “Vancouver developers are sensing that the market is on the upswing. Total marketing starts are up by about 18 per cent from the second half of 2010,” MPC reported. Total condo apartment and townhome sales in new projects in 2011 are expected to rise by about 10 per cent from 2010 and a whopping 73 per cent higher than in 2009, MPC forecasts. Is the new-condo market on a roll again? “We believe that the gains made over the past 12 to 18 months will be temporary. Recent improvement in new-condo sales have benefitted from the release of pent-up demand from the 2008-09 period. Further gains in sales will depend on household growth in Metro Vancouver. [But] the latest net migration figures show growth is slowing,” warned MPC. According to MPC, the real threat to a sustained recovery of the new-condo market will be an oversupply of new product, especially in areas of the Fraser Valley. “We expect a push of new product in the fall of 2011 as developers look to capitalize on current market conditions,” MPC stated. The hottest new-condo market, according to MPC, is East Vancouver. “Perhaps the best opportunities for new low rise over the next 12 months; sales could increase by 35 per cent to 40 per cent if new product is available. Even with the average price-per-square foot at $535, prices could increase by 6 per cent.” The challenging markets for strata developers include North Surrey, South Surrey and Langley, all of which are facing a possible oversupply of new condos. Asian factor With a surprising 44 per cent drop in immigration to B.C. during the first quarter of this year, the Asian factor is becoming a hotter topic since many developers are aiming product precisely at this sector. Asia has a fascination for Vancouver. Decades of migration and the influx of Hong Kong buyers during the 1980s keep the city looking west across the Pacific. The latest wave is driven by Canada’s designation by China as an approved destination for travellers and Beijing’s imposition of restrictions on domestic investment following China’s unrivalled economic boom. “There are certainly more Chinese buyers today than there were two years ago,” said Daryl Simpson, vice-president, sales and marketing, with Bosa Properties Inc. “They’re looking for a change of place, or a second or third residence around the world where they feel comfortable, safe and secure.” The influx is taking Chinese buyers well beyond the neighbourhoods they’ve traditionally scouted for properties, contributing to a perception that buyers from Mainland China are dominating the market. Bulk-buy myth “They are looking further afield than they traditionally looked. They’re looking beyond Richmond, the West Side and Metrotown,” Simpson said. “You’re seeing that in North Vancouver, you’re seeing it in Coquitlam, you’re seeing it in White Rock.” Viceroy, a 170-unit project Bosa launched in New Westminster this past May, had sold 82 homes by the end of July. Of these, about half sold to Chinese buyers. “Chinese buyers in uptown New Westminster? That’s unheard of,” Simpson said with amazement. He cautioned against painting them all with the same brush, however. “Chinese buyers don’t all have this homogenous motivation. They’re just like you and me,” Simpson said. “When people hear ‘Chinese investors’ they think all Chinese investors are buying with the same motivation. That they’re all buying it to either flip it, or they’re all buying it to rent it out or they’re all buying it to sit empty for three years until they move here, or they’re buying it for a child that’s going to go to UBC. [But] they’re buying it for all those reasons and others.” The perspective is backed up by some common measures of investor activity in Vancouver. Statistics from BC Hydro regarding power consumption below the minimum threshold established for occupied apartments have typically pegged vacant downtown condos at about 8 per cent of the total stock. This year, BC Hydro numbers pegged the proportion of vacant units city-wide at 2.4 per cent of low-rise units and 3.9 per cent of highrise apartments. Of course, many foreign-owned apartments might be rented out, so a lack of power consumption isn’t the best measure of foreign ownership. But even then, speaking to the Urban Development Institute in May 2011, condo marketer Bob Rennie observed that for the Lower Mainland as a whole, 2,500 condos are foreign-owned (or approximately 1.2 per cent) based on where assessment notices are sent. And foreign buyers of single-family homes are equally few, at just 607 (or 0.15 per cent of the regional total). Another measure comes from MAC Marketing Solutions, which issued a report in June noting that of 500 buyers surveyed in the first five months of this year, just three listed an address in China as their primary residence. Follow the money But Jeff Hancock of MPC Intelligence said that even if this is the case, Chinese money is what’s driving sales and developers know it. “You start asking [developers] where their deposit cheques are coming from, and you start seeing a huge proportion of their deposit cheques are coming straight from China,” Hancock said. He says no one measure will effectively track buyer origins, but it’s clear that offshore buyers are an important component of the Vancouver – and British Columbia – market. “Make no mistake,” Hancock said of offshore buyers, “they are driving the new-home market.” Simpson agrees: “Developers now are looking at immigration statistics as often as we’re looking at mortgage rates,” he said. “For a developer in Vancouver not to be in tune with what’s happening with Asian immigration is foolish.” Western Investor September 2011