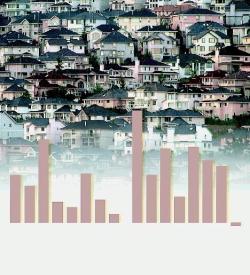

In past 10 years, other cities have fared better than Vancouver

Sun

CREDIT: Graphic: Vancouver Sun; Source: Century 21 VANCOUVER: POINT OF LOW RETURN: A new survey by Century 21 Canada shows that a highly indebted Greater Vancouver homeowner might have actually lost money on his or her property investment in the last 10 years. The same highly indebted homeowner might have made money in Greater Vancouver in the last five years, but he or she would have fared better in any other major Canadian market in terms of percentage return on investment.

The way the housing market is going these days, homeowners in Greater Vancouver are feeling pretty good about their investments right now.

But if you take a look at the 10-year return the way you might look at a mutual fund’s performance, a home in the city has been a pretty lousy investment.

In fact, if you bought a home in Vancouver 10 years ago with $20,000 down, chances are you would have actually lost money — an average of 13 per cent — after paying all the interest on your mortgage, according to a survey released Monday by Century 21 Canada.

Even if you bought the home outright, the positive 60-per-cent return was the lowest of all 20 Canadian cities Century 21 surveyed, and less than half the 131 per cent you would have made investing the same amount of money in the Toronto Stock Exchange composite index instead.

The smart money was in smaller centres — would you believe Halifax-Dartmouth? With a $20,000 downpayment, someone who bought there in 1994 would have increased their equity 436 per cent. Or a homebuyer could have made 431 per cent on their investment in Peterborough, Ont.

The secret to investing in real estate is timing, especially when doing so with the bank’s money, explained Century 21 president Don Lawby. In 1994, Vancouver home prices were high, and falling in real terms (adjusted for inflation) off their 1989 peak. In most of Canada they were already beginning to turn around.

“The Vancouver market only started to turn four years ago,” he said. And later still in the rest of B.C.

As a result, a house or condominium in the city performed better as an investment over the past five years, with a 50-per-cent return for a buyer putting $20,000 down, or 49 per cent for someone paying cash up front.

A buyer in the Okanagan Mainline real estate district (which includes Kelowna and Vernon) would have done better still, earning a 203-per-cent return on $20,000 invested, or 71 per cent on the full value of the house over five years.

Of the big cities, Ottawa was the place to be, with an average 512-per-cent return on equity since 1999, and 287 per cent since 1994 for those carrying a mortgage.

While most real estate surveys look only at the change in average home prices, Century 21 decided to factor in the cost of financing because “that’s how most people invest in real estate,” Lawby said.

“People gather as big a downpayment as they can, and then they buy a house, leveraging their investment by borrowing money from the bank. So, when they sell the house, they don’t just earn a return on their downpayment; they earn a return on the full sale price of the house.”

The Richmond-based real estate company examined the growth of $20,000 invested in an average home as a downpayment, subtracting mortgage payments at prevailing five-year rates and adding in “imputed rent” (what the buyer would otherwise have to pay for a two-bedroom apartment in the same market) over the course of the five- and 10-year periods. Then it figured what would be left over if you sold the home today and paid off the remaining mortgage principal.

Vancouver was the only place where there was less than $20,000 left over at the end of 10 years.

In the low-interest-rate environment of the past few years, carrying a big mortgage could serve to increase the return on your original investment — the downpayment — faster than owning a home outright. But leveraging can work against homeowners when interest rates rise or when home prices decline. That was the situation for heavily indebted Vancouver homeowners in the mid-1990s.

The good news is that means the Greater Vancouver home prices have probably yet to reach their peak, Lawby said.

“I think there’s an upside” to buying a home in the city now, he said. Although long-term mortgage rates have begun to rise again, rates are still close to historical lows and the economy is growing. The conditions that led to a market bust in 1989 — speculative buying by investors, the onset of recession and the Bank of Canada’s raising the overnight rate three-quarters of a percentage point in one go — are nowhere in sight.

Lawby says home prices in B.C. will continue to rise for “at least the balance of this year.” The big question mark for 2005 is a provincial election, he said.

The time to reconsider carrying a big mortgage is when interest rates are rising fast or when you start hearing bad things about the economy.

“People start talking about recessions a lot sooner than governments come out with the numbers,” he said.

Prospective buyers should also understand that there is no such thing as an average home. Homes will appreciate differently depending on the neighbourhood, age and condition, and the supply and demand for a particular kind of property.

Lawby conceded he did not do particularly well buying a White Rock condominium, which turned out to have leaks.

“Other than that, I would have done okay,” he jokes.

© The Vancouver Sun 2004